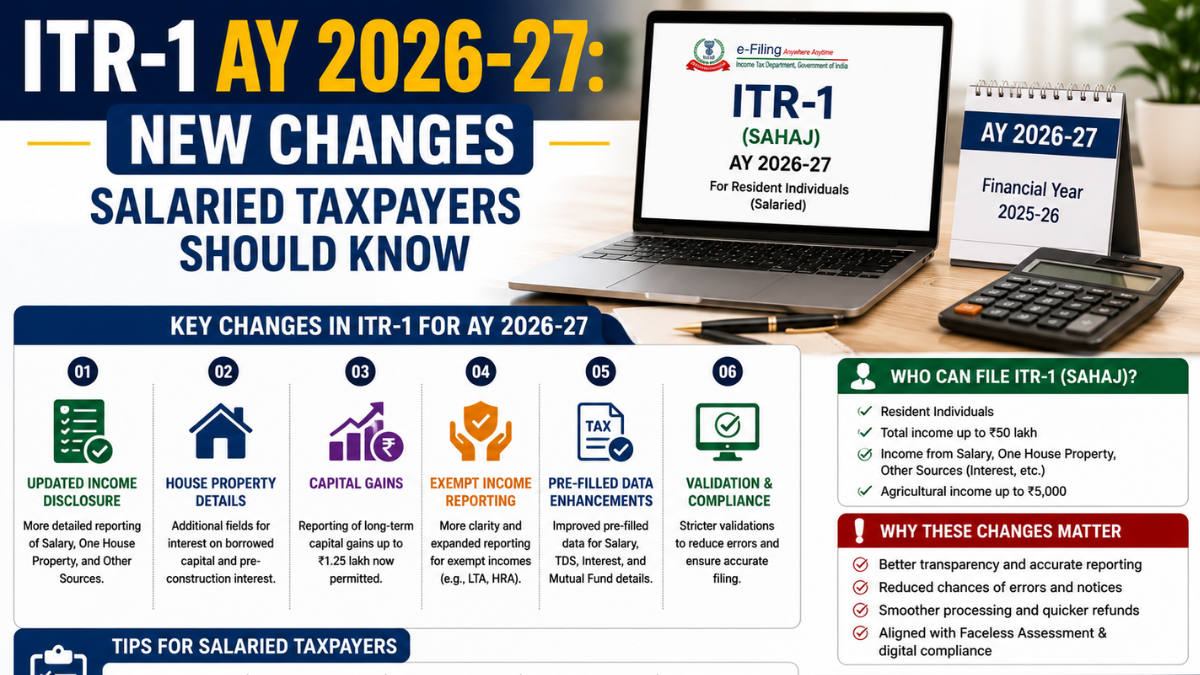

ITR-1 AY 2026-27 has become more useful for salaried taxpayers because the form now covers more situations than before. The Income Tax Department’s official notification for AY 2026-27 describes ITR-1 as applicable to resident individuals with total income up to ₹50 lakh from salary, two house properties, other sources, Section 112A long-term capital gains up to ₹1.25 lakh and agricultural income up to ₹5,000.

This is a genuine filing relief for many salaried taxpayers who earlier had to shift to ITR-2 because of a second house property or small listed-equity LTCG. But do not assume ITR-1 is now open for everyone. The form is still simple only for taxpayers whose income sources fit the permitted categories.

What Are The Big Changes?

The biggest changes are around house property reporting and LTCG reporting. ITR-1 can now be used by eligible taxpayers having income from up to two house properties, and it also allows reporting of long-term capital gains under Section 112A up to ₹1.25 lakh, subject to conditions. The Income Tax portal has also enabled ITR-1 and ITR-4 filing utilities for AY 2026-27.

| Change | What It Means |

|---|---|

| Two house properties | Eligible taxpayers can use ITR-1 even with income from two houses |

| LTCG under Section 112A | Allowed up to ₹1.25 lakh |

| Income limit | Total income must be up to ₹50 lakh |

| Agricultural income | Allowed up to ₹5,000 |

| Filing utility | ITR-1 online and Excel utility are live |

This is where many taxpayers will make mistakes. Two house properties do not mean unlimited property complexity, and LTCG up to ₹1.25 lakh does not mean every capital-gains case can use ITR-1. If you have short-term capital gains, higher LTCG or carried-forward losses, ITR-1 may not be the right form.

Who Can File ITR-1?

ITR-1 is mainly for resident individuals, other than not ordinarily resident, whose total income is up to ₹50 lakh and comes from permitted sources. The Income Tax portal’s salaried-individual guidance lists salary or pension, house property, other sources, agricultural income up to ₹5,000 and Section 112A capital-gain income up to ₹1.25 lakh among the covered areas.

Common eligible cases include:

- Salaried employees with Form 16

- Pensioners with interest income

- Taxpayers with up to two house properties

- Small dividend or bank interest income

- Section 112A LTCG up to ₹1.25 lakh

- Agricultural income up to ₹5,000

The smart move is to check eligibility before filing, not after getting an error or notice. If your income source is even slightly complicated, forcing ITR-1 just because it looks easier is a bad idea. A wrong form can create defects, delays and correction work.

Who Cannot Use ITR-1?

ITR-1 cannot be used by every salaried person. The Income Tax portal says ITR-1 cannot be used by a person who is a company director, has short-term capital gain, has Section 112A LTCG exceeding ₹1.25 lakh, held unlisted equity shares during the previous year or falls under other excluded categories.

Taxpayers with foreign assets, foreign income, business or professional income, crypto income, more complex capital gains or carried-forward losses should be careful. The blunt truth is simple: choosing the wrong ITR form to save five minutes can create months of tax compliance headache. Simplicity is useful only when it is legally correct.

What Should Salaried Taxpayers Check?

Salaried taxpayers should not file immediately just because the utility is live. First, they should match Form 16, Form 26AS, AIS, bank interest, dividend income, rent income and capital-gain statements. If Section 112A gains are involved, they should verify the amount carefully before deciding whether ITR-1 is allowed.

Before filing, check these items:

- Form 16 from employer

- AIS and Form 26AS tax credit

- Bank interest and FD interest

- Rent from house property

- Home loan interest details

- Listed equity or mutual fund LTCG

- Deductions under old tax regime, if chosen

The biggest blind spot is AIS mismatch. Many taxpayers file only from Form 16 and ignore interest, dividend or capital-gain data already visible to the department. That is careless because pre-filled data may not be perfect, but ignoring it completely is worse.

What Is The Deadline?

For salaried and other non-audit taxpayers using ITR-1, the commonly reported due date for AY 2026-27 filing is July 31, 2026. Economic Times reported that taxpayers filing ITR-1 for AY 2026-27 need to file on or before July 31, 2026, to avoid penalties.

Do not wait until the last week unless you enjoy portal pressure, missing documents and panic filing. Filing early gives you time to correct mismatches, verify refund details and avoid avoidable mistakes. Tax filing is not difficult, but lazy preparation makes it painful.

Conclusion?

ITR-1 AY 2026-27 brings real relief for eligible salaried taxpayers because it now covers two house properties and Section 112A LTCG up to ₹1.25 lakh. The filing utility is live, and taxpayers can start preparing their return after checking Form 16, AIS, Form 26AS and income details carefully.

The honest takeaway is simple: ITR-1 is easier, but it is not universal. If your income is simple and within the allowed limits, use it confidently. If you have excluded income or complicated gains, do not force the wrong form. Correct filing matters more than quick filing.

FAQs?

What Are The Main ITR-1 AY 2026-27 Changes?

The major changes are that eligible taxpayers can report income from up to two house properties and Section 112A long-term capital gains up to ₹1.25 lakh in ITR-1. The income limit remains ₹50 lakh for eligible resident individuals.

Can I File ITR-1 With Two House Properties?

Yes, eligible taxpayers can file ITR-1 with income from up to two house properties for AY 2026-27. However, other eligibility conditions must also be satisfied before using the form.

Can ITR-1 Be Used For Capital Gains?

ITR-1 can be used only for Section 112A long-term capital gains up to ₹1.25 lakh, subject to conditions. If you have short-term capital gains or LTCG above the limit, ITR-1 is not suitable.

What Is The ITR-1 Filing Last Date For AY 2026-27?

The commonly reported due date for ITR-1 filing by non-audit taxpayers for AY 2026-27 is July 31, 2026. Taxpayers should file early after checking Form 16, AIS and Form 26AS.