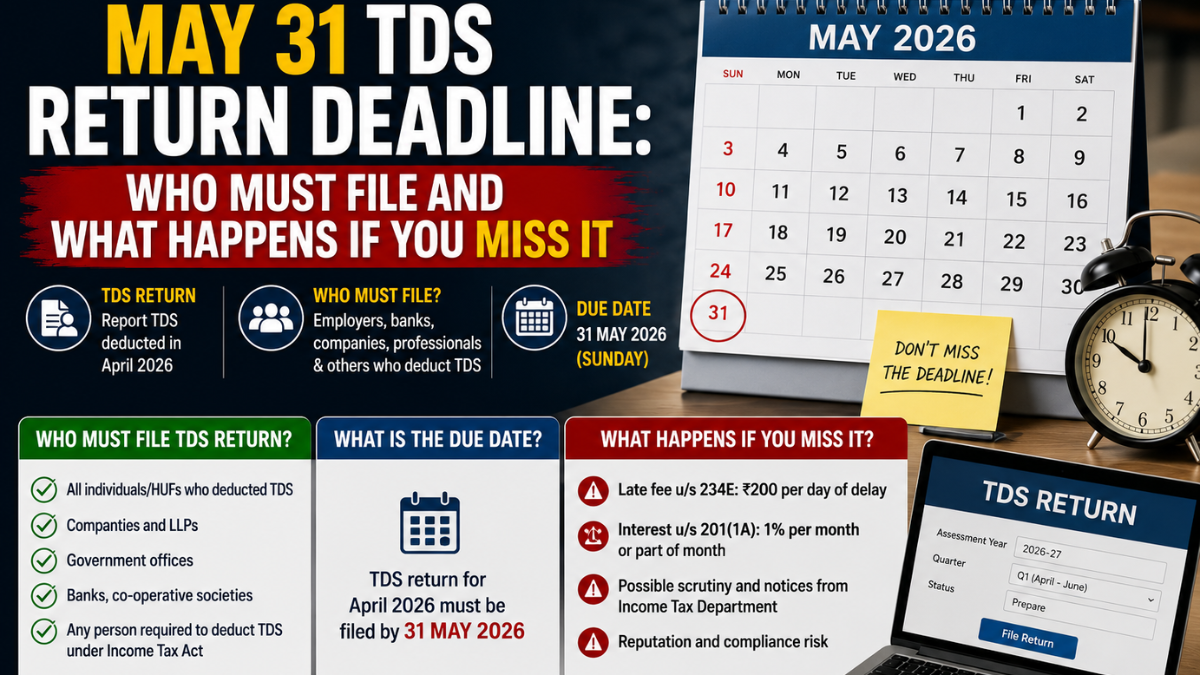

May 31 TDS return deadline is important because deductors must file the quarterly TDS statement for the quarter ending March 31, 2026. This is the last quarter of FY 2025-26, and it directly affects the tax-credit records of employees, vendors, contractors, professionals and other deductees. The Income Tax Department’s tax calendar lists May 31, 2026, as the due date for the quarterly statement of TDS deposited for the quarter ending March 31, 2026.

This deadline should not be treated like routine paperwork. If the TDS return is delayed or filed incorrectly, deductees may not see proper credit in Form 26AS or AIS, creating problems when they file their ITR. The blunt truth is simple: one careless deductor can create tax trouble for many people.

Who Must File TDS Return?

Any person or entity that deducted TDS during the quarter must generally file the applicable TDS statement. This includes employers deducting salary TDS, businesses deducting tax on contractor payments, professional fees, rent, commission, interest and other specified payments. The exact form depends on the nature of deduction.

| TDS Form | Common Use |

|---|---|

| Form 24Q | Salary TDS |

| Form 26Q | Non-salary resident payments |

| Form 27Q | Payments to non-residents |

| Form 27EQ | TCS statement |

| Q4 Due Date | May 31, 2026 |

Businesses should not assume that depositing TDS is enough. Payment and return filing are separate compliance steps. If tax is deposited but the quarterly statement is not filed, the deductee may still face credit mismatch, and the deductor may face late filing consequences.

What Happens If You Miss It?

If the TDS/TCS statement is not filed by the due date, Section 234E late fee can apply. ClearTax explains that late filing of TDS/TCS statements attracts a fee of ₹200 per day until the return is filed, but the fee cannot exceed the total TDS/TCS amount.

There can also be a penalty under Section 271H for late or incorrect filing. ClearTax notes that the assessing officer may levy a penalty from ₹10,000 to ₹1,00,000 under Section 271H, including where incorrect details are furnished.

What Errors Create Trouble?

Late filing is not the only problem. Incorrect PAN, wrong challan details, mismatch in deduction amount, wrong assessment year, incorrect section code and missing deductee entries can also create serious issues. These mistakes can block tax credit even when the money has already been deducted and deposited.

Common mistakes to avoid:

- Wrong PAN or name mismatch

- Incorrect challan serial number

- Wrong TDS section selected

- Salary and non-salary data mixed incorrectly

- Deducted amount not matching challan

- Return filed without proper reconciliation

The worst habit is filing in a hurry on the last day without checking data. That is not efficiency; it is carelessness. A clean return is better than a rushed return that later needs correction and creates unnecessary notices or deductee complaints.

Why Does Form 26AS Matter?

Form 26AS and AIS show tax deducted against a taxpayer’s PAN. If the deductor files the TDS return correctly, the deductee can claim that credit while filing ITR. If the return is missing, delayed or wrong, the deductee may see lower credit and may be asked to pay tax again until the mismatch is fixed.

This is why TDS return filing is not just the deductor’s internal compliance. It affects employees, vendors, landlords, consultants and taxpayers who depend on accurate reporting. A business that delays TDS filing is not only risking penalty; it is damaging trust with people whose tax has already been deducted.

What Should Deductors Do Now?

Deductors should immediately reconcile books, challans and deductee-wise TDS details before filing the Q4 statement. They should verify PAN details, payment sections, deduction dates, challan amounts and return form selection. If the return has already been filed, they should download acknowledgement and check whether any correction is needed.

Quick action checklist:

- Match ledger TDS with challan payments

- Verify deductee PAN before filing

- Check correct form: 24Q, 26Q or 27Q

- Review salary and non-salary sections separately

- Save acknowledgement after filing

- Correct mistakes quickly if found later

Do not wait for deductees to complain after checking Form 26AS. That is a reactive and weak way to manage compliance. Serious businesses verify their TDS records before the deadline and keep proof ready for audit and future reference.

Conclusion?

May 31 TDS return deadline is crucial for the Q4 statement for FY 2025-26. Deductors must file the quarterly TDS return for the period ending March 31, 2026, and ensure that all challans, PAN details, deduction amounts and sections are correctly reported. Missing the deadline can trigger late fees and possible penalty exposure.

The honest advice is simple: do not treat TDS return filing as clerical work. It affects tax credit, ITR filing, vendor trust and compliance history. File on time, reconcile properly and fix errors quickly. Tax mistakes look small until they become notices, penalties and angry deductees.

FAQs?

What Is The May 31 TDS Return Deadline?

May 31, 2026, is the deadline for filing the quarterly TDS statement for the quarter ending March 31, 2026. It is mainly relevant for deductors who deducted TDS during Q4 of FY 2025-26.

Who Must File TDS Return By May 31?

Employers, businesses, firms and other deductors who deducted tax during the January to March quarter must file the applicable TDS return. The form depends on whether the deduction relates to salary, non-salary resident payments or non-resident payments.

What Is The Late Fee For Missing TDS Return Deadline?

Late filing can attract a fee of ₹200 per day under Section 234E until the return is filed. The fee cannot exceed the total TDS/TCS amount for the statement.

Can Wrong TDS Return Be Corrected Later?

Yes, correction statements can be filed for mistakes such as wrong PAN, challan mismatch or incorrect deduction details. However, deductors should correct errors quickly because wrong reporting can block deductees’ tax credit in Form 26AS or AIS.